If you are active in the energy sector you probably heard already about flexibility. At the high level, flexibility is defined as the ability of an energy system to respond to changes in supply and demand. Of course an increasing share of intermittent renewable energy in the supply side adds flexibility requirements in the system in order to remain balanced at any point in time. Belgian TSO Elia approximates Belgian energy system to require an additional 3GW of flexibility, up and down, in the next 5 to 10 years.

In the frame of this article we will focus on flexibility at the supply (production) side. Adjusting energy production to balance the grid is nothing new. Natural gaz power plants or storage batteries are already actively balancing the grid. It is however the fact that while solar energy causes significant share of imbalance on the grid, it is currently not bringing its fair share of flexibility into the system. And for good reasons as piloting solar power plant output requires a significant technological stack.

The following lines describe techniques, approximate returns and assess maturity of flexibility sources for solar energy.

Returns are computed on a period of 12 months from October 2023 to September 2024.

The very first strategy to bring flexibility to a solar power plant is to completely shut down production when day-ahead electricity (spot) prices are negative. This is pretty straightforward as a simple curtailment of the inverter will do the trick. Spot prices are by definition available in advance so you will hardly get it wrong.

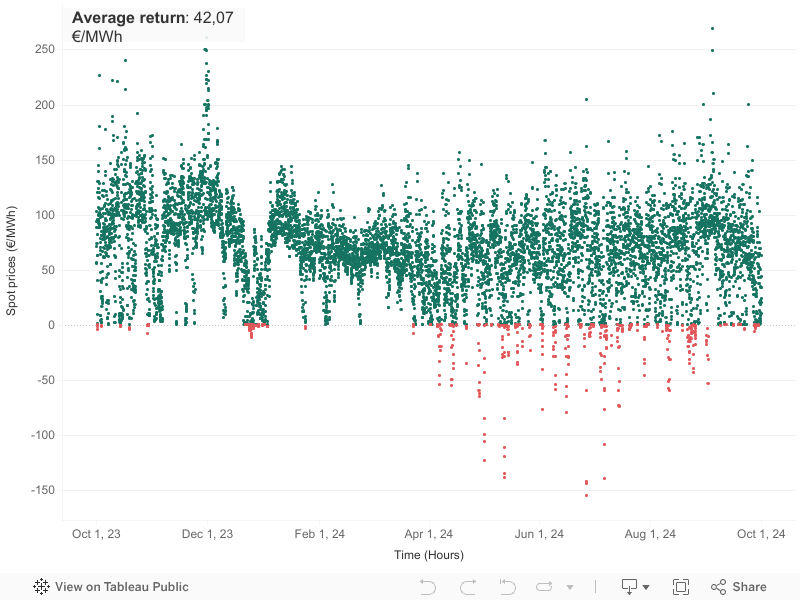

Spot prices

Spot price evolution in Belgium, Elia

Simple curtailment of inverters during negative spot prices increases profitability by 10.6% going from 38,02 €/MWh to 42,07 €/MWh. While this effectively bring flexibility into the system, it exclusively translates into avoiding revenue reduction for solar power plant owners.

Next strategy for solar flexibility is to combine spot injections with participation in the imbalance price market. In this strategy you will need to predict imbalance prices throughout the day as it changes depending on the current level of unbalance on the grid.

Imbalance price distribution is detailed in the post: “The rise of solar capacity“.

Imbalance price predictions methodologies and performances are detailed in next post: “Imbalance price market and solar energy“.

As a solar power plant owner, there are two ways of doing this. The first one is to mandate a BSP to deal with your solar output. It will include it into its global energy pool and direct it to the imbalance price as part of the a global portfolio strategy. You will then receive a profit sharing from the BSP that mostly depends on your contract.

While it results in extra profits for solar power plants, it does not exactly bring flexibility to the system as it mostly redirects produced energy from one market to another with no piloting of solar injections.

The second way is to expose solar production to imbalance prices directly at the injection endpoint. The solar power plant is responsible for nominations and deviations. While this approach is not widely implemented, it is gaining momentum as IoT and forecasting techniques are building up. Further, it reacts to imbalance price evolution and effectively brings flexibility to the system. This approach will be detailed in next post “Imbalance price market and solar energy“.

Following strategy bringing flexibility to solar power plants is to couple it with storage battery systems. First incentive is to increase auto-consumption by storing excessive generated power. Second incentive is to store solar generated power to trade it on imbalance price market afterwards. PV-battery coupling is estimated to increase solar power plant profitability from 38,02 €/MWh to 120 €/MWh. Moreover it adds effective flexibility into the system.

The main inconvenient here is the battery acquisition price. Battery capacity needs to approach plant capacity for this strategy to make sense. A kW of battery is currently more expansive than a kW of solar capacity. Moreover storage batteries usually have shorter lifespan. Therefore it might not exactly fit the purpose of the solar power plant developer. Stand alone, higher scale, energy market trading storage batteries have recently been quiet profitable, but it is another topic.

A final strategy is to combine spot injections with participation in aFRR markets. aFRR markets are organised by national TSO and intend to offer energy availability to level up our level down energy in the system when the grid is unbalanced. Any energy provider/consumer can take part to this market. Balance responsible parties (BSPs) are the ones contracting with the TSO.

A more detailed description of capacity market is provided by Next Kraftwerken here: https://www.next-kraftwerke.com/tag/grid-balancing

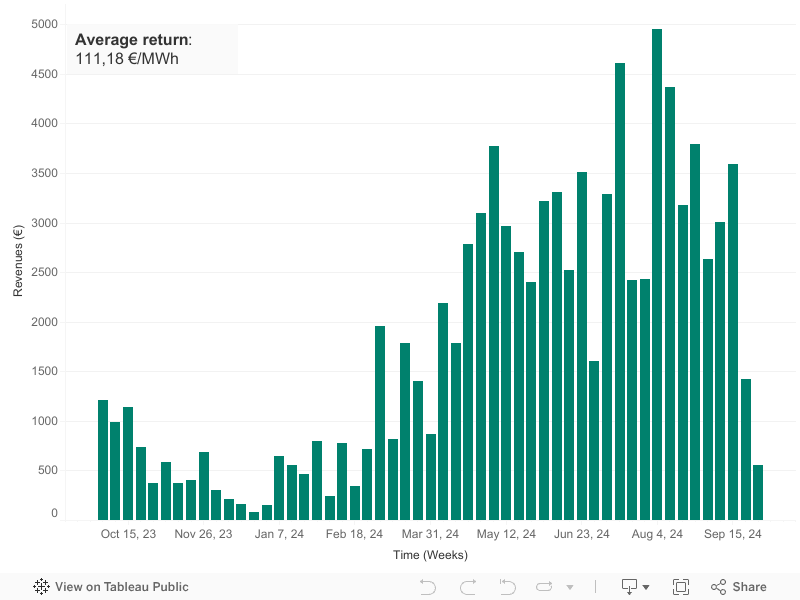

Spot injections and aFRR downward activations

Revenues for spot injections and aFRR downward activations strategy for a 1 MWp solar power plant based in Brussels, Epon Energy

Combining spot prices with aFRR down activations raise solar power profitability from 38,02 €/MWh to 111,18 €/MWh .

The strategy effectively brings flexibility into the system. Further it tends to bring the grid exactly what it expects from solar power. Indeed downward capacity incentives tend to be high when spot prices are to low. Piloting solar power plant reactively to aFRR down prices would enable our national solar capacity to rise by keeping incompressibility stresses at bay.

This approach however requires baselining of solar output and accurate prediction of solar production at the local level. It is currently not properly implemented for solar power plants but machine learning and AI developments are making big steps towards first proof of concepts.

The post “Steady the solar profile with accurate forecasting” details technological developments supporting this strategy.